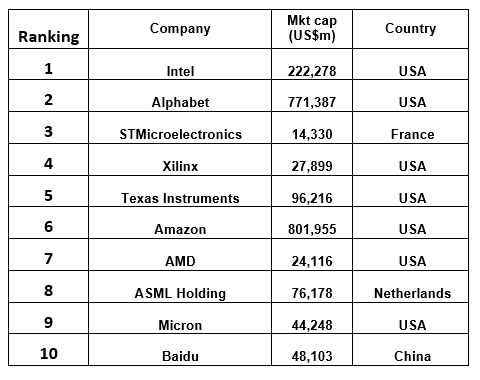

Intel is the company which is best placed to succeed in the semiconductor sector, according to exclusive theme-based analysis.

GlobalData has scored the world’s top 57 semiconductor companies on their leadership in the 10 themes which matter most for the industry. These companies comprise the leading listed chip designers, foundries, semiconductor equipment companies and integrated device manufacturers.

Go deeper with GlobalData

The top themes disrupting the semiconductor industry have been defined as the following (with the % weighting given to them in brackets) :

• Data centres (15%)

• High-performance computing (15%)

• Artificial intelligence (15%)

• Ambient commerce (10%)

• Self -driving cars (10%)

• Industrial Internet (10%)

• M&A (10%)

• Gaming (5%)

• 5G (5%)

• Geopolitics (5%).

Intel has been ranked as a leader in most of these areas meaning it is likely to perform well in the future. In second place was Google parent company Alphabet followed by France-based STMicroelectronics.

The GlobalData Thematic Screen ranks companies within a sector on the basis of overall technology leadership in the ten themes that matter most to their industry, generating a leading indicator of future earnings growth.

Five predictions around disruptive industry themes

Data centres and memory chips

An enormous amount of research and development (R&D) spending goes towards memory chip research. By 2022 a new class of hybrid memory will arrive that combines the best of dynamic random access memory (DRAM), speed, with the persistence of flash memory. It will move much closer to the processor and help tackle storage density and access speed issues. Established players like Intel, Samsung, Micron, and SK Hynix are competing in R&D terms against agile newcomers like Everspin.

Leading chip makers: Samsung, SK Hynix, Toshiba, Intel, Micron, Western Digital.

Artificial intelligence (AI) and algorithmic chips

There is a high degree of specialisation among available acceleration chip architectures, each focusing on solving performance problems specific to different use cases, deployment environments, and even phases of the AI application lifecycle (modelling, training, inference, optimisation, etc.). This specialisation and the popularity of AI itself has led to an arms race among chip manufacturers seeking to solve both narrow and wide AI problems on mobile devices, at the network edge, in the data centre and on the public cloud platform.

Leaders: Intel, Google, Microsoft, Amazon, Apple, Alibaba, Baidu, Nvidia, AMD, Xilinx, Tesla and Huawei.

Autonomous vehicles

Over the next couple of years, demand for chips from the auto sector will rise significantly. Google’s Waymo, the leading developer of the ‘robot driver,’ is based on hardware from Intel/Mobileye, while Nvidia, Baidu, and start-up Aurora are gaining considerable traction, with Nvidia leading the way. Apple, with its Titan project, is very much the dark horse. Tesla is developing its own AI chip. China is investing in scores of AI chip start-ups focused on supplying and developing this sector.

Leading auto chip suppliers: NXP, STMicro, Infineon, Mobileye (Intel), AMS, Renesas, Melexis, Nvidia and Bosch.

M&A

China’s intention to acquire a chip industry by buying US assets has been thwarted by an implacable Committee on Foreign Investment in the United States (CFIUS).

This turn of events is likely to see China return to intellectual property (IP) theft, and to personnel and technology transfer to build a world-class native chip industry. The apex chip companies, within an already radically shrunken global chip industry, are still looking for ways to use M&A to cut costs, round out R&D resources, extend product lines but most of all acquire scarce design and AI talent. Intel, for example, has almost certainly not finished its acquisition run, while Broadcom, which acquired software company CA Technologies in 2018, is still on the hunt as semiconductor shares slump.

Texas Instruments is a dark horse having not made an acquisition since 2011 when it bought National Semiconductor.

Industrial Internet of Things

Microcontrollers and sensors – including accelerometers, heat and humidity components, pressure components, cameras, and microphones – will be where much of the value lies in 2019. This calls for industrial grade chips that work to higher reliability standards than chips for consumer applications.

Leaders: AMS, Analog Devices, STMicro, NXP, Infineon, Renesas, Rohm, Broadcom, Intel, Microchip, Qualcomm, Qorvo and Skyworks.

What is the GlobalData Thematic scorecard?

The GlobalData Thematic Research ecosystem is a single, integrated global research platform that provides an easy-to-use framework for tracking all themes across all companies in all sectors.

From Coca-Cola to Cisco; from Tesco to Thomson-Reuters, their awareness of or susceptibility to disruptive themes – from AI to e-commerce or Big Data to Brexit – is what will make or break them.

The scorecard is the methodology that not only tells savvy CEOs across every sector what themes they should be aware of, it also tells them which suppliers they can trust to help them survive disruptive change. Its ‘screen of truth’ identifies not today’s incumbents, but tomorrow’s leaders and laggards.

Research methodology

Our thematic scores are based on our analysts’ assessment of their competitive position in relation to a theme, on a scale of 1 to 5:

1. Vulnerable: The company’s activity with regards to this theme will be highly detrimental to its future performance.

2. Follower: The company’s activity with regards to this theme will be detrimental to its future performance.

3. Neutral: The company’s activity with regards to this theme will have a negligible impact on the company’s future performance, or this theme is not currently relevant for this company.

4. Leader: The company is a market leader in this theme. The company’s activity with regards to this theme will improve its future performance.

5. Dominant: The company is a dominant player in this theme. The company’s activity with regards to this theme will significantly improve its future performance.